Today is the deadline for U.S. citizens to pay their taxes. What should they know about crypto taxation?

Depending on what country you live in, your cryptocurrency will be subject to different tax rules. The questions below address implications within the United States, but similar issues arise around the world. As always, check with a local tax professional to assess your own particular tax situation.

1. Do I need to report my cryptocurrency trades to the IRS?

You need to report your cryptocurrency activity if you incurred a taxable event during the year. A taxable event is a specific scenario that triggers a tax liability. The below are a list of the taxable events as specified by the IRS 2014 guidance:

- Trading cryptocurrency to fiat currency like the U.S. dollar is a taxable event.

- Trading cryptocurrency to cryptocurrency is a taxable event (you have to calculate the fair market value in USD at the time of the trade).

- Using cryptocurrency for goods and services is a taxable event (again, you have to calculate the fair market value in USD at the time of the trade; you may also end up owing sales tax).

The most common tax event from the above is trading one cryptocurrency for another — for example, trading your Bitcoin (BTC) for Ethereum (ETH).

On the other hand, there are other actions that cryptocurrency enthusiasts also commonly take that are not taxable events and do not trigger a tax reporting requirement. Listed below are scenarios in which traders do not trigger a tax event:

- Giving cryptocurrency as a gift is not a taxable event (the recipient inherits the cost basis; the gift tax still applies, if you exceed the gift tax exemption amount).

- A wallet-to-wallet transfer is not a taxable event (you can transfer between exchanges or wallets without realizing capital gains and losses, so make sure to check your records against the records of your exchanges, because they may count transfers as taxable events, like they are a safe harbor).

- Buying cryptocurrency with USD is not a taxable event. You don’t realize gains until you trade, use or sell your crypto. If you hold longer than a year, you can realize long-term capital gains (which are about half the rate of short-term). If you hold less than a year, you realize short-term capital gains and losses.

An example

Let’s say you buy 2 BTC from Coinbase. You just hold this crypto for the year. In this case, you have no reporting requirement, as you have not triggered a taxable event. Even if you send this to an offline wallet, you still do not need to report this, as merely sending crypto from one place to another is not a taxable event.

Now let’s say you send this 2 BTC to Binance and start trading it for other altcoins. Now you have incurred a taxable event (trading one cryptocurrency for another) and you will need to report this transaction on your taxes and file it with your 2018 tax return, even if you lost money on the trade.

Keep in mind that mining cryptocurrency is also taxable and is treated as income.

2. How do I file my crypto taxes?

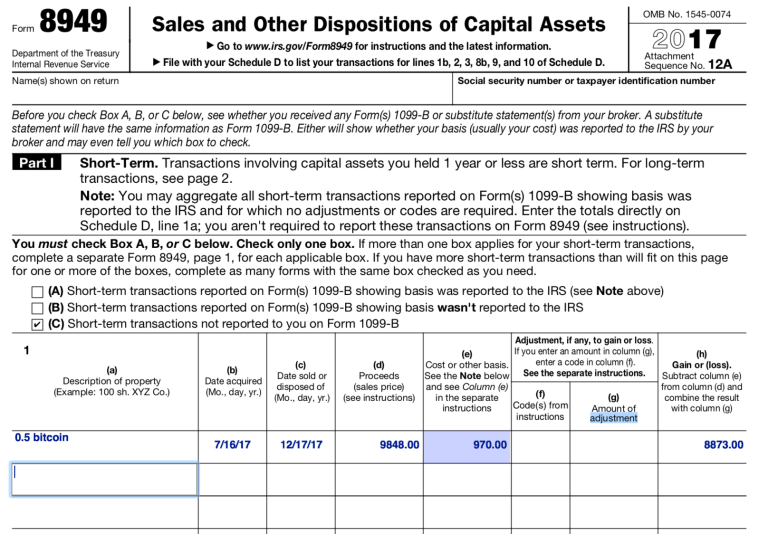

If you are simply buying, selling and trading cryptocurrencies you will report these trades on the IRS Form 8949, as pictured below.

As seen in the above example, you have sold 0.5 Bitcoin. You acquired the Bitcoin on July 16, 2017, and you sold it on December 17, 2017. You sold the Bitcoin for a total proceed of $9,848.00, and your cost basis was $970.00. This led to your gain of $8,873.00 (reported in column h).

You will report each crypto-to-crypto trade and each taxable event from the calendar year on this form.

You can use crypto tax software to automatically build this report for you, if you don’t have your own records of the historical prices, dates and fair market values of your trades.

Once you have your net gain or loss calculated from Form 8949, the total will simply flow into your 1040 Schedule D. You should include these forms with your entire tax return upon filing.

Foreign account holdings

If you traded on foreign exchanges like Binance, you may additionally need to report these holdings. You do not pay any tax on these holdings, but it is important that you file the following reports if either situation applies to you.

FBAR: A taxpayer with a financial interest in or signatory authority over a foreign financial account must file a Foreign Bank Account Report (FBAR) FinCEN Form 114 if the aggregate value of the foreign financial account exceeds $10,000 at any time during the calendar year. Noncompliance with FBAR would subject a taxpayer to steep civil and criminal penalties. Each nonwillful failure-to-file violation can carry a civil penalty of $10,000. Penalties for each willful violation could be the greater of $100,000 or 50% of the amount in the account.

FATCA: A taxpayer with foreign financial assets of $50,000 or more must report it under Foreign Account Tax Compliance Act (FATCA) requirements on Form 8938. It is recommended that cryptocurrency-invested hedge fund accounts and cryptocurrency-denominated exchange accounts be reported in the summary information in Part I of Form 8938. Specific information should be given in Part V. Noncompliance with FATCA could subject a taxpayer to taxes, severe penalties in excess of the unreported foreign assets, and exclusion from access to U.S. markets, which could include a regulated cryptocurrency derivatives clearing market.

3. What will happen if I don’t report my crypto activity?

The reality is that no one knows for sure. However, it is not advised.

The IRS publicly stated on July 2, 2018 that one of their core campaigns and focuses for the year is the taxation of virtual currencies. Unfortunately, lack of reporting will be treated as tax fraud.

4. Can I reduce my tax bill by filing my crypto capital losses?

Yes.

When you realize a capital gain — if you sold your crypto for more than you purchased it for — you owe a tax on the dollar amount of the gain. However, when you sell (or trade) your crypto for less than you purchased it for, you incur a capital loss, and you can use this loss to offset gains from other trades or even a gain from the sale of other property — like stocks in your portfolio.

Whenever your total capital gains and losses for the year add up to a negative number, you incur a net capital loss. If the net capital loss is less than or equal to $3,000 ($1,500 if you are married and filing a separate tax return), then that entire capital loss can be used to offset other types of income — like the income from your job.

If your losses exceed $3,000, then the amount over $3,000 will be rolled forward to the next tax year.

The bright spot in the 2018 bear market is that your losses can reduce your tax bill.

5. Why can’t I get my tax documents from the exchanges that I use?

Cryptocurrency exchanges are unable to provide their users with accurate tax documentation. This is a big problem in the industry.

By the nature of the blockchain technology that exchanges operate on, users are able to send Bitcoin and other cryptocurrencies to wallet addresses outside of their own network. An example of this would look like you buying Bitcoin through Coinbase and then sending it to a Binance wallet address in order to acquire new coins and assets on Binance that Coinbase does not offer.

Because you can send cryptocurrencies from other platforms onto exchanges like Coinbase at any time, Coinbase has no possible way of knowing how, when, where or at what cost you acquired that cryptocurrency that you sent in. Coinbase only sees that it showed up in your Coinbase wallet.

This means that anytime you move crypto assets off of Coinbase or into Coinbase from another location, Coinbase completely loses the ability to provide you with accurate tax information. This is because it has no way of identifying what your cost basis is in that certain cryptocurrency, which is an essential piece to figure out your capital gain or loss. This is also true of all other major cryptocurrency exchanges.

The solution to this problem is to leverage crypto tax aggregating tools to collect your data from all platforms to build your holistic tax reports.

David Kemmerer is the co-founder of CryptoTrader.Tax, cryptocurrency-focused tax software for automating your tax reporting.

from Cointelegraph.com News http://bit.ly/2UDZgpA

No comments:

Post a Comment